Emerging markets to lead global growth in 2017

Global growth expected to pick up but downside risks remain

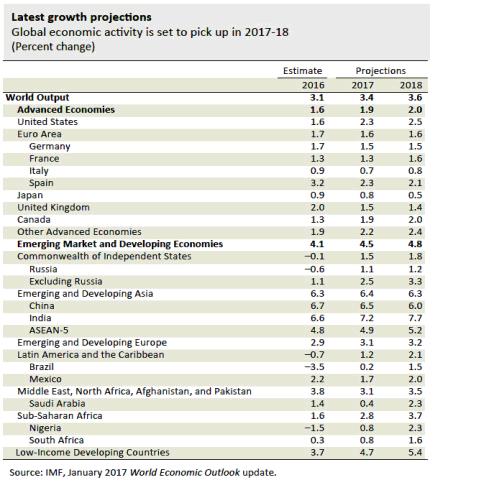

Emerging markets, led by India and China, are expected to continue to lead global growth in 2017 – according to the International Monetary Fund’s (IMF) January 2017 update to the World Economic Outlook.

In a recent release[i], the global financial watchdog notes that developments since last summer indicate somewhat greater growth momentum coming into the New Year in a number of important economies such as China, Japan and the United States.

But at the same time, it sees a wider dispersion of risks to its forecast, with the risks tilted to the downside in the wake of rising uncertainty.

The IMF projects that global growth will rise to 3.4% in 2017 and 3.6% in 2018, up from a 3.1% in 2016. “Much of the better growth performance we expect this year and next stems from improvements in some large emerging market and low income economies that in 2016 were exceptionally stressed, “ it states.

Emerging and developing economies are forecast to grow by 4.5% in 2017 and 4.8% in 2018, up from 4.1% in 2016. India is expected to grow by 7.2% and 7.7%, respectively, in 2017 and 2018; while China is projected to grow by 6.5% in 2017 but slow down to 6% in 2018.

But “China remains a major driver of world economic developments. Our China growth upgrade for 2017 is a key factor underpinning the coming year’s expected faster global recovery,” states the IMF.

The IMF’s China stance “reflects an expectation of continuing policy support; but a sharp or disruptive slowdown in the future remains a risk given continuing rapid credit expansion, impaired corporate debts, and persistent government support for inefficient state-owned firms.”

According to the IMF, optimism about stronger global growth[ii] stems from:

Broad indicators of manufacturing activity in emerging and advanced economies have been in expansionary territory and rising since early summer (2016).

In many countries, previous downward pressures on headline inflation weakened, in part owing to firming commodity prices.

A significant re-pricing of assets followed the U.S. presidential election. The most notable elements include a sharp increase in U.S. longer-term interest rates, equity market appreciation and higher long-term inflation expectations in advanced economies, and sharp movements in opposite directions of the dollar—up—and the yen—down. At the same time, emerging market equity markets broadly retreated as currencies weakened.

Incidentally, most commentators have interpreted the post-election moves as predicting that U.S. fiscal policy will turn more expansionary and require a swifter pace of interest rate increases by the Federal Reserve. Markets have noted that the White House and Congress are in the hands of the same party for the first time in six years, and that change points to lower tax rates and possibly higher infrastructure and defense spending.

Risks[iii]

There is thus a wider than usual range of upside and downside risks to this forecast. A sustained non-inflationary growth increase, marked by higher labor force participation and significant expansion of the U.S. capital stock and infrastructure, would allow a more moderate pace of interest rate increases in line with the Federal Reserve’s price stability mandate.

On the downside, if a fiscally-driven demand increase collides with more rigid capacity constraints, a steeper path for interest rates will be necessary to contain inflation, the dollar will appreciate sharply, real growth will be lower, budget pressure will increase, and the U.S. current account deficit will widen.

This last scenario, one with a widening of global imbalances, intensifies the risk of protectionist measures and retaliatory responses. It would also imply a faster than expected tightening of global financial conditions, with resulting possible stress on many emerging market and some low-income economies. Some emerging and especially low-income commodity exporters could benefit from higher export prices, but importers would then lose. The details of the U.S. policy mix matter; and as these become clearer, we will adjust our forecast and spillover assessment.

At the global level, other vulnerabilities include higher popular antipathy toward trade, immigration, and multilateral engagement in the United States and Europe; widespread high levels of public and private debt; ongoing climate change—which especially affects low-income countries; and, in a number of advanced countries, continuing slow growth and deflationary pressures. In Europe, Britain’s terms of exit from the European Union remain unsettled and the upcoming national electoral calendar is crowded, with possibilities of adverse economic repercussions, in the short and longer terms.

[i] https://blog-imfdirect.imf.org/2017/01/16/a-shifting-global-economic-landscape-update-to-the-world-economic-outlook/

[ii] ibid

[iii] ibid

Related Articles

Views from on-the ground experts at the Excel Emerging Markets Symposium

Below are summaries from the recent Excel Emerging Markets Symposium. Mahesh Patil India, leading the world in growth Mr. Richard

Emerging Markets Race Ahead in January

Emerging market equities were off to a strong start overall in 2019, rebounding from a 2018 downturn. Manraj Sekhon, CIO

The Leapfrog: The Role of Technology in Accelerating Emerging Markets’ Growth

The potential for emerging and frontier markets to realize accelerated economic growth as a result of new technology transfer comes