Financial inclusion efforts in Mexico give way to new market highs

Global investors might not be aware that Mexico’s stock market has been rising to new heights this year. Dina Ting, Head of Index Portfolio Management, Franklin Templeton ETFs, makes the case to consider adding some exposure.

Mexican stocks have reached new highs this year. The FTSE Mexico RIC Capped Index is up more than 26% year-to-date, with consumer staples and materials constituents leading the way higher.1

There are a few factors buoying the positive sentiment. We’ve seen reshoring and nearshoring booms that have taken advantage of the country’s geographical supply chain benefits and competitive rates for highly skilled labor, along with the country’s recent progress in increasing access to financial services.

With more international companies establishing manufacturing in Mexico or relocating manufacturing there, the country’s industrial park occupancy hit a record high last year. US firms accounted for approximately 45% of investments into such facilities,2 but global firms based in other regions have also contributed to the uptick. For example, out of 40 new industrial park projects managed by the Mexican Association of Private Industrial Parks, 52% are linked to China, followed by Italy at 13% and Germany at 8%.3

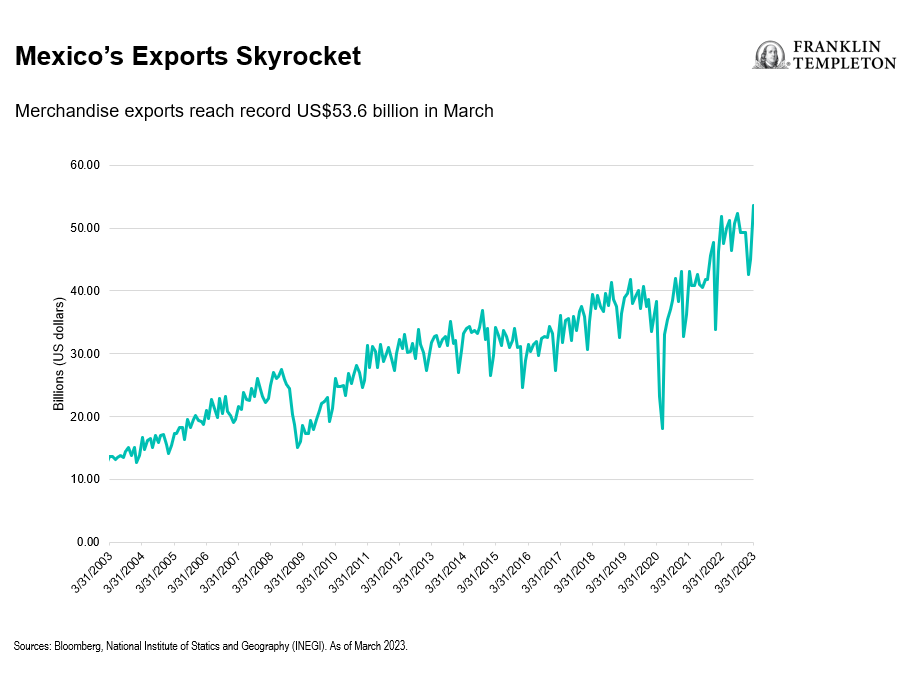

In addition, strong North American demand for Mexican goods led to a better-than-expected trade surplus in March, when the country’s exports reached a record US$53.6 billion.

Investors seeking targeted exposure to a broad swath of companies in Mexico, including the notable fintech and retailing segments, can consider single-country exchange-traded funds (ETFs) for flexible and low-cost access to the country’s equities. ETFs, which have democratized the investing experience, allow access to strategies and entire asset classes that were previously only available to larger institutional investors. They also provide opportunities to target outcomes through tactical country allocations.

Democratizing financial inclusion

Some consumer staples firms in Mexico’s stock market have been recent standouts. Tapping into the change that is underway in the payments space, some retailers are now playing a greater role in financial inclusion efforts through the rollout of alternative payment methods. For example, one of Latin America’s largest beverage and retail giants based in Mexico is leveraging access to customers of its ubiquitous convenience store chains with new digital debit cards that may help financial services penetration—a central government priority.

The opportunity set is great, in our view. Mexico is the region’s largest economy to remain heavily cash based. In 2021, only 20% of the country’s adults reported having a department store credit card, and that figure was double the percentage who reported owning a bank credit card.4

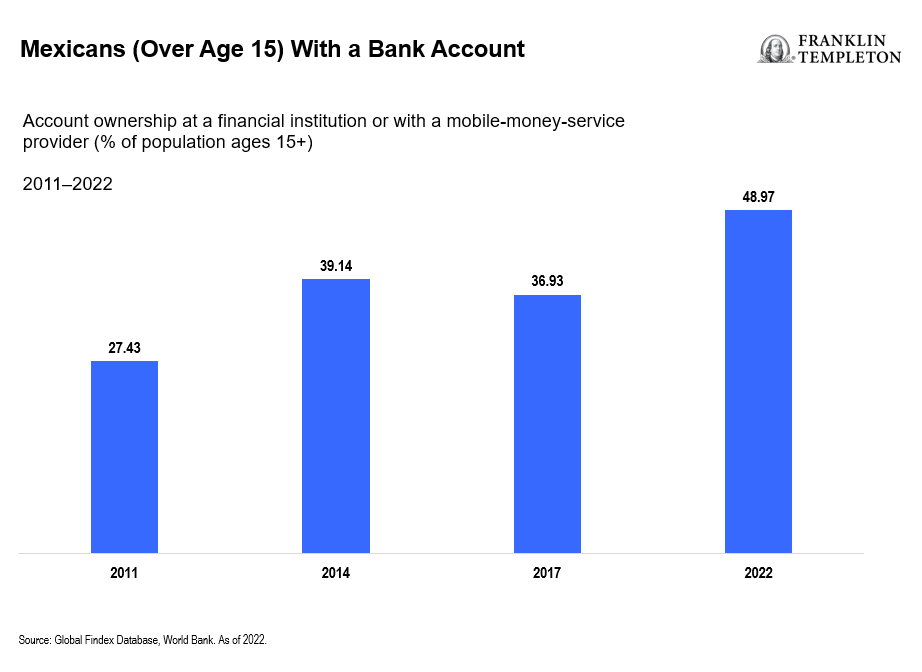

Other new programs from Mexico’s retailers may offer products for remittances, loans to small businesses, and other traditional services. These efforts are widely seen as a positive for the country’s nascent digital economy. There is much room for growth, in our assessment, as only about 49% of individuals over the age of 15 held a bank account in 2022, up from 37% in 2017, according to the World Bank.

Mexico is part of a free-trade area that allows its industry to integrate into North American supply chains. Yet its challenges still include a stubbornly high poverty rate of roughly 40%,5 along with more than 55%6 of its workforce and many businesses making up its informal labor force, which means, they do not fulfill tax obligations or make social-insurance contributions.

Certain analysts point to other hefty challenges that remain, particularly among Mexico’s smaller cities and rural areas. “Citizens in three-quarters of Mexico’s municipalities do not have even one access point for financial services within a two-kilometer walk,” said former International Monetary Fund (IMF) Director Christine Lagarde during a 2019 speech in Mexico City. “When it comes to replacing cash as a means of payment, Mexico lags . . . . ”7

Mere months before the COVID-19 pandemic began, however, Mexican officials made strides in modernizing the country’s financial systems and regulations. They passed new legislation to promote and enhance fintech solutions and launched initiatives to bolster financial literary education in schools. By many accounts, Mexico’s fintech ecosystem is flourishing, owing to the country’s market attractiveness, high smartphone and internet penetration, and improvements in debit-card and digital-wallet usage.

In mid-May 2023, Mexico’s central bank joined other Latin American central banks in halting their monetary tightening cycles, and its efforts to tame inflation have been helped by the peso, a top-performing currency against the US dollar among emerging markets this year. Given this backdrop and the current global market environment, we believe Mexico may offer good potential opportunity for investors, particularly for those looking to add emerging market exposure to their portfolios.

WHAT ARE THE RISKS?

All investments involve risks, including the possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in developing markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity.

Any companies and/or case studies referenced herein are used solely for illustrative purposes; any investment may or may not be currently held by any portfolio advised by Franklin Templeton. The information provided is not a recommendation or individual investment advice for any particular security, strategy, or investment product and is not an indication of the trading intent of any Franklin Templeton managed portfolio.

ETFs trade like stocks, fluctuate in market value and may trade above or below the ETF’s net asset value. Brokerage commissions and ETF expenses will reduce returns. ETF shares may be bought or sold throughout the day at their market price on the exchange on which they are listed. However, there can be no guarantee that an active trading market for ETF shares will be developed or maintained or that their listing will continue or remain unchanged. While the shares of ETFs are tradable on secondary markets, they may not readily trade in all market conditions and may trade at significant discounts in periods of market stress.

Commissions, management fees, brokerage fees and expenses may be associated with investments in ETFs. Please read the prospectus and ETF facts before investing. ETFs are not guaranteed, their values change frequently, and past performance may not be repeated.

Past performance is not an indicator or guarantee of future performance. There is no assurance that any estimate, forecast or projection will be realised.

Links to External Sites

Franklin Templeton is not responsible for the content of external websites.

The inclusion of a link to an external website should not be understood to be an endorsement of that website or the site’s owners (or their products/services).

Links can take you to third-party sites/media with information and services not reviewed or endorsed by us. We urge you to review the privacy, security, terms of use, and other policies of each site you visit as we have no control over, and assume no responsibility or liability for them.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice. This material may not be reproduced, distributed or published without prior written permission from Franklin Templeton.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The underlying assumptions and these views are subject to change based on market and other conditions and may differ from other portfolio managers or of the firm as a whole. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. There is no assurance that any prediction, projection or forecast on the economy, stock market, bond market or the economic trends of the markets will be realised. The value of investments and the income from them can go down as well as up and you may not get back the full amount that you invested. Past performance is not necessarily indicative nor a guarantee of future performance. All investments involve risks, including possible loss of principal.

Any research and analysis contained in this material has been procured by Franklin Templeton for its own purposes and may be acted upon in that connection and, as such, is provided to you incidentally. Data from third party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. Although information has been obtained from sources that Franklin Templeton believes to be reliable, no guarantee can be given as to its accuracy and such information may be incomplete or condensed and may be subject to change at any time without notice. The mention of any individual securities should neither constitute nor be construed as a recommendation to purchase, hold or sell any securities, and the information provided regarding such individual securities (if any) is not a sufficient basis upon which to make an investment decision. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

________________________

1. Source: Bloomberg, as of May 16, 2023. Indexes are unmanaged and one cannot directly invest in them. They do not include fees, expenses or sales charges. Past performance is not an indicator or guarantee of future results.

2. Source: Grupo Financiero Banorte, February 15, 2023.

3. Ibid.

4. Sources: CNBV; Scotiabank GBM. As of 2021.

5. Source: International Monetary Fund.

6. Source: Statista. “Informal employment as percentage of total employment in Mexico from 1st quarter 2015 to 4th quarter 2022.“

7. Source: International Monetary Fund, “Mexico: An Opportunity for Financial Inclusion,” May 29, 2019.

Related Articles

EM Intelligence Exclusive: Why Emerging Markets Now?

Given the relative importance of emerging markets which account for over 30% of total absolute global equity market capitalization, it

A Few Words on Greece

Greece’s ongoing debate about the best way forward has now played out at the ballot box, although many uncertainties remain.

Emerging Markets Race Ahead in January

Emerging market equities were off to a strong start overall in 2019, rebounding from a 2018 downturn. Manraj Sekhon, CIO