Kuwait’s Emerging Markets Arrival Signals New Era of Investment

Kuwait’s upgrade to index provider MSCI’s Emerging Markets Index puts the Middle East and North Africa (MENA) region firmly on the global investment map, according to Bassel Khatoun and Salah Shamma, Franklin Templeton Emerging Markets Equity. They consider the potential asset flows this move could bring, and weigh in on the opportunities they see for Kuwait and the wider MENA region.

Kuwait stands on the cusp of a new era of investment. Its promotion to the MSCI Emerging Market (EM) Index this week puts the country in the cross hairs of deep pocketed global investors and roughly US$1.8 trillion that tracks the popular gauge.1 The upgrade is contingent on the introduction of a number of new regulatory mechanisms affecting international institutional investors before November.

The significant liquidity surge that typically accompanies emerging-market promotion also means investors in Kuwait could find opportunities from a more institutionalized and liquid stock market.

Kuwait’s MSCI upgrade reflects the hard work that the country’s Capital Markets Authority has undertaken over the past two years to make its stock market more accessible and attractive to global investors. During this time, it has made tangible improvements to its clearing, custody, and settlement services, increased foreign ownership levels (FOL) and eased the process of setting up investor trading accounts.

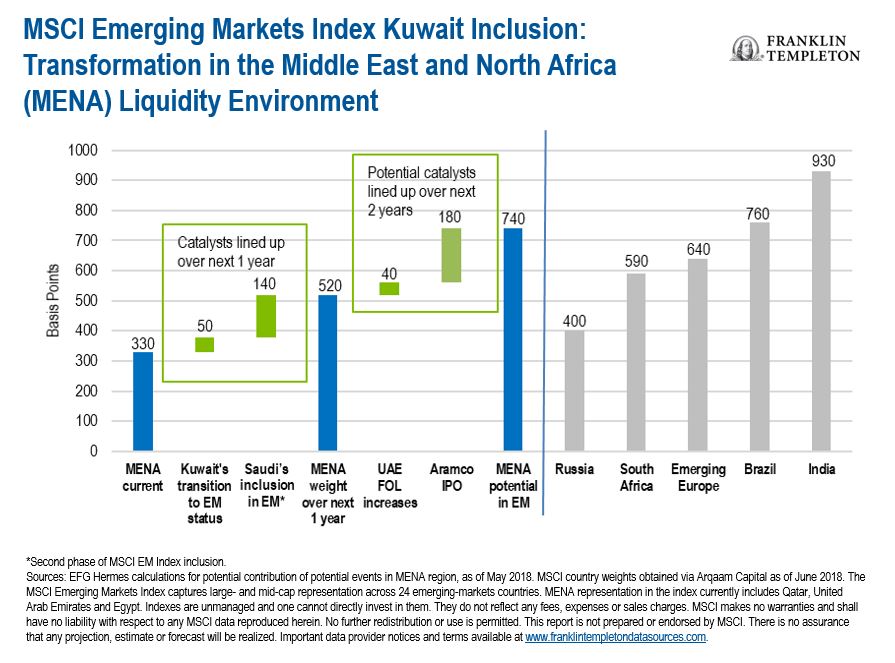

According to MSCI, up to 18 Kuwaiti stocks will be eligible for the MSCI EM Index, with the inclusion basket likely to be concentrated in banks (c.70%).2 Actual implementation, however, will not take place until May 2020. While Kuwait has already been recognized as an emerging market by rival index providers FTSE Russell (FTSE EM) and S&P Dow Jones, the country’s inclusion in MSCI’s EM Index is a landmark deal and should represent Kuwait’s biggest-ever liquidity event.

Initially, Kuwait’s MSCI EM weighting might amount to approximately 50 basis points, or 0.5%.3Based on this representation, we anticipate likely total investor flows of about US$10 billion (US$2.5 billion in passive flows and US$7.5 billion in potential active flows).4 For context, over the past 12 months Kuwait has seen a total of US$1.9 billion of foreign inflows, driven primarily by the FTSE EM Index inclusion which took place over two phases in September and December 2018.5

Attractive Fundamentals Still Drive Kuwait’s Story

Upgrades aside, the fundamental case for investing in Kuwait may be worth considering. With substantial reserves, low levels of debt and a stable banking sector, Kuwait stands out in an emerging market context. When one adds to this a budget breakeven oil price of just US$49 a barrel for 2019 (the lowest by some margin in the region) and a “AA” credit rating by Moody’s, Kuwait could be considered a low beta, defensive investment destination.6

Another factor in Kuwait’s growing appeal is its diversification story that’s gaining momentum. Kuwait continues to make significant progress in terms of fiscal and structural reforms and is committed to developing a dynamic and vibrant private sector. And while there is still some way to go, the results of Kuwait’s move to reduce the role of the public sector in the economy are encouraging, in our view.

The country is moving away from oil dependence by developing its infrastructure, investing in human capital and promoting private sector involvement. In the government’s Vision 2035 plan, it has developed a blueprint for a more sustainable future. To date, we’ve seen about US$60 billion of investment allocated under this plan, with the prospect of $100 billion more to come, providing an ample runway for growth. When you consider that Kuwait’s Northern Gulf Gateway project alone is expected to add about US$220 billion to Kuwait’s gross domestic product.

In our view, there is also a solid valuation argument to be made for Kuwaiti stocks. Despite trading at a 15% premium to emerging market peers, valuations remain reasonable. It is worth keeping in mind that the surge in liquidity that will likely accompany Kuwait’s MSCI EM inclusion does have the potential to stretch valuations further. Recent upgrades of the United Arab Emirates (UAE), Qatar, Pakistan and Saudi Arabia increased valuations significantly in the final year prior to inclusion.

Moreover, we believe the earnings outlook for listed Kuwaiti companies supports a valuation premium. On average, Kuwait stocks are delivering 13.5% earnings per share growth coupled with a 4.8% dividend yield which is attractive within an emerging market context.7 On a sector view, we remain particularly upbeat about Kuwait’s banking sector, which is showing improving profitability on the back of falling provisioning and improving asset quality.

Our view is that with Kuwait’s addition to the MSCI EM Index, combined with Middle East and North Africa (MENA)8 representation, will amount to approximately 5.2%, putting this region firmly on the global investment map.9 We would also expect more active money managers begin to look at the MSCI EM Index through a MENA lens, raising the possibility of a positive spillover impact for the region’s capital markets.

We believe Kuwait’s MSCI promotion is just reward for the range of transformational measures it has implemented to improve its capital markets. And although the pace and quantum of change in the country has, in the past, been slower than neighbors like the UAE and Saudi Arabia, Kuwait’s encouraging fundamentals should likely draw additional interest from emerging market investors.

Important Legal Information

The comments, opinions and analyses presented herein are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy. Past performance is not an indicator or guarantee of future results.

Data from third-party sources may have been used in the preparation of this material and Franklin Templeton (“FT”) has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information, and reliance upon the comments, opinions and analyses in the material is at the sole discretion of the user. Products, services and information may not be available in all jurisdictions and are offered by FT affiliates and/or their distributors as local laws and regulations permit. Please consult your own professional adviser for further information on availability of products and services in your jurisdiction

What Are the Risks?

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

_________________________________________________________________________

1. Source: MSCI, June 2019.The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-markets countries. MENA representation in the index currently includes Qatar, United Arab Emirates and Egypt. Indexes are unmanaged and one cannot directly invest in them. They do not reflect any fees, expenses or sales charges. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com.

2. Source: MSCI, June 2019.

3. Franklin Templeton internal estimate, June 2019. There is no assurance that any estimate, forecast or projection will be realized.

4. Ibid.

5. Kuwait Stock Exchange, June 2019.

6. Source: Moody’s Investor Service. According to Moody’s, obligations rated AA are judged to be of high quality and are subject to very low credit risk. In the world of investing, beta has traditionally been a measure of a security’s or portfolio’s volatility in comparison to the stock market as a whole. Today, the word “beta” is also used as shorthand to describe getting broad stock-market exposure, typically through investments that often track the S&P 500 and other major indexes.

7. Bloomberg, June 2019.

8. The Middle East and North Africa region includes Kuwait, Saudi Arabia, UAE, Qatar and Egypt.

9. MSCI, Franklin Templeton internal estimate, June 2019. There is no assurance that any estimate, forecast or projection will be realized.

Bassel Khatoun

Chief Investment Officer, MENA Equities

Franklin Local Asset Management – MENA