Emerging markets continued to struggle in October amid an environment of heightened equity-market volatility globally. Manraj Sekhon, CIO of Franklin Templeton Emerging Markets Equity, and Chetan Sehgal, senior managing director and director of portfolio management, believe the pullback presents long-term investors with opportunities amid what they dub an overreaction. They present the team’s overview of the emerging-markets universe in October.

Three Things We’re Thinking about Today

1. Jair Bolsonaro emerged victorious in Brazil’s presidential election, solidifying investors’ optimism for a more market-friendly policy approach. Looking forward, we believe this should be positive for earnings growth and for the Brazilian equity market generally. Political stability could also result in a more favorable climate where consumer and business confidence can pick up again and lead to an acceleration in domestic economic activity. The local market is trading at what we view to be reasonable price-earnings levels and should have more scope for improvement as the economic situation improves. Initiatives such as pension reform and an acceleration in privatization could also be expected under the next president as part of efforts to tackle the deficit, improve the efficiency of the state-owned companies and lower corporate taxes.

2.We believe China’s near-term downside risk from an equity market perspective may be limited given the recent correction, whereas the upside on the positive resolution of trade issues and execution of reform initiatives could be significant. We are of the opinion that China has the policy tools to manage economic challenges and provide stimulus as it continues with structural reforms. We saw regulators implement a number of measures, including a 1% cut in banks’ reserve requirement ratio, an increase in export tax rebates and tax deductions on household income, in October. Moreover, China offers an unparalleled range of investment opportunities as rapid digitalization and growing consumption support growth for companies across different industries. Accordingly, when we look at the valuations and earnings potential of Chinese companies, underlying strength in the Chinese economy and ongoing reform efforts, we remain optimistic for China’s long-term potential.

3. Pessimism about future global growth, the US-China trade conflict, rising US interest rates and a strengthening US dollar have led emerging market (EM) investors to switch to more defensive stocks in recent months. October saw technology-related stocks record double-digit declines, while the utilities and telecommunication services sectors fared much better. However, we think the market reaction has been excessive. We believe areas such as e-commerce, digital banking and mobile computing will likely be fundamental drivers of the global economy for years to come. EMs’ accelerating internet usage and penetration are likewise hastening opportunities for efficiencies, cost savings and ease of doing business. Promising fields such as artificial intelligence, autonomous driving and the Internet-of-Things continue to attract investment, signaling strong prospects.

Outlook

We are of the opinion that the market has been discounting a far more pessimistic scenario than we currently envisage for emerging markets. EM fundamentals remain strong and we believe that the recent selloff provides attractive investment opportunities for long-term investors.

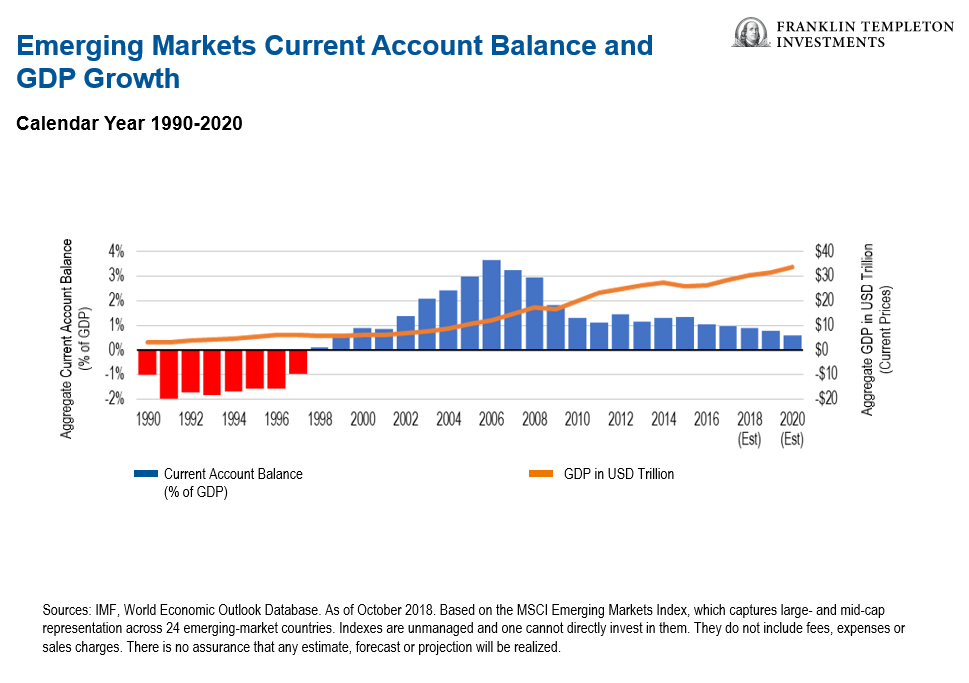

We do not expect contagion from markets such as Turkey and Argentina to spread across the entire EM asset class. The fact is that this is a very different world from past crises: most emerging countries have floating exchange rates, current account surpluses and more favorable debt levels than their developed market peers. Moreover, Turkey accounts for less than 1% of the MSCI Emerging Markets Index, while Argentina is not in the index, and its weighting is expected to be even smaller than Turkey’s when it is included in 2019.

In terms of US-China trade concerns, China’s dependency on trade has been declining, and trade with the United States represents a modest percentage of the Chinese economy. Moreover, intra-EM trade has become more important in recent years, and rising tariffs between the United States and China may further pivot focus toward greater regional agreements. For example, tensions between China and Japan have started to ease, resulting in Japanese Prime Minister Shinzo Abe visiting China in October to discuss increased co-operation, the first such trip by a Japanese prime minister since 2011. The long-term structural case for EMs continues to center around demographics, consumption and technological advances. We believe that the best investment results are achieved by buying companies which have sustainable earning power and trade at a discount to their intrinsic worth.

Emerging Markets Key Trends and Developments

A combination of headwinds sent global stocks lower in October, with EM equities ceding more ground than their developed-market (DM) counterparts. Concerns about global economic growth, prospects for major technology companies, US interest rate hikes, and US-China trade tensions curbed investor sentiment. The MSCI Emerging Markets Index fell 8.7% over the month, compared with a 7.3% decline in the MSCI World Index, both in US dollars.1

Asian stocks registered broad-based losses. South Korea and Taiwan led the way down, as their technology-heavy indexes fell amid a rout in global technology stocks. China’s stock market was also among the weakest performers in the region, hampered by slowing domestic economic growth and fears of an escalation in the US-China trade dispute. Measures from the Chinese authorities to support the economy helped stem the market’s decline. However, the Philippines and Indonesia fared relatively better, albeit also ending October in negative territory.

Latin America was the only EM region to end the month with a positive return, solely because of the strong performance of the Brazilian market. Equity prices rallied on expectations for, and the subsequent victory of, a more market-friendly candidate in presidential elections late in the month as well as appreciation in the Brazilian real. At the other end of the spectrum, Mexico and Colombia recorded double-digit declines. The cancelation of the new Mexico City Airport project and expectations that persistent inflation could result in higher interest rates impacted investor sentiment in Mexico. A decline in oil prices and depreciation in the Colombian peso weighed on the Colombian market.

Emerging European markets corrected in October, but performed better than their EM peers. Poland, Greece and the Czech Republic fell the most. Eurozone worries weighed on the region in October following fiscal concerns and a credit downgrade in Italy, as well as German Chancellor Angela Merkel’s decision not to run for a fifth term. The Russian market also corrected on the back of lower oil prices. A strong appreciation in the Turkish lira partially offset losses in US-dollar terms in that market. In South Africa, stocks in the consumer discretionary, materials and financials sectors declined the most.

Although frontier markets as a group declined, they outperformed their EM and DM counterparts. Kazakhstan, Lebanon and Sri Lanka were among the top-performing markets, ending the month with positive returns. The Moscow Exchange (MOEX) and Kazakhstan Stock Exchange (KASE) signed a strategic partnership agreement in October, which also included plans for the MOEX to acquire a 20% stake in the KASE. Hopes that a political upheaval in Sri Lanka could result in a more-growth focused government boosted sentiment in that market. Lithuania and Vietnam, however, underperformed.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The comments, opinions and analyses expressed herein are solely the views of the author(s), are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

Important Legal Information

All investments involve risks, including the possible loss of principal. Investments in foreign securities involve special risks including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions.

_________________________

1. Source: MSCI. The MSCI Emerging Markets Index captures large- and mid-cap representation across 24 emerging-market countries. The MSCI World Index The MSCI World Index captures large- and mid-cap performance across 23 developed markets. Indexes are unmanaged and one cannot directly invest in them. MSCI makes no warranties and shall have no liability with respect to any MSCI data reproduced herein. No further redistribution or use is permitted. This report is not prepared or endorsed by MSCI. Important data provider notices and terms available at www.franklintempletondatasources.com. Past performance is not an indicator or guarantee of future performance.